Life Insurance for Young Adults: A Comprehensive Guide

Life insurance is often associated with older individuals who have dependents and mortgages to consider. However, young adults can also benefit greatly from having life insurance coverage. In this comprehensive guide, we will explore the importance of life insurance for young adults, the types of coverage available, factors to consider when choosing a policy, and tips for finding the best life insurance plan that suits your needs and budget.

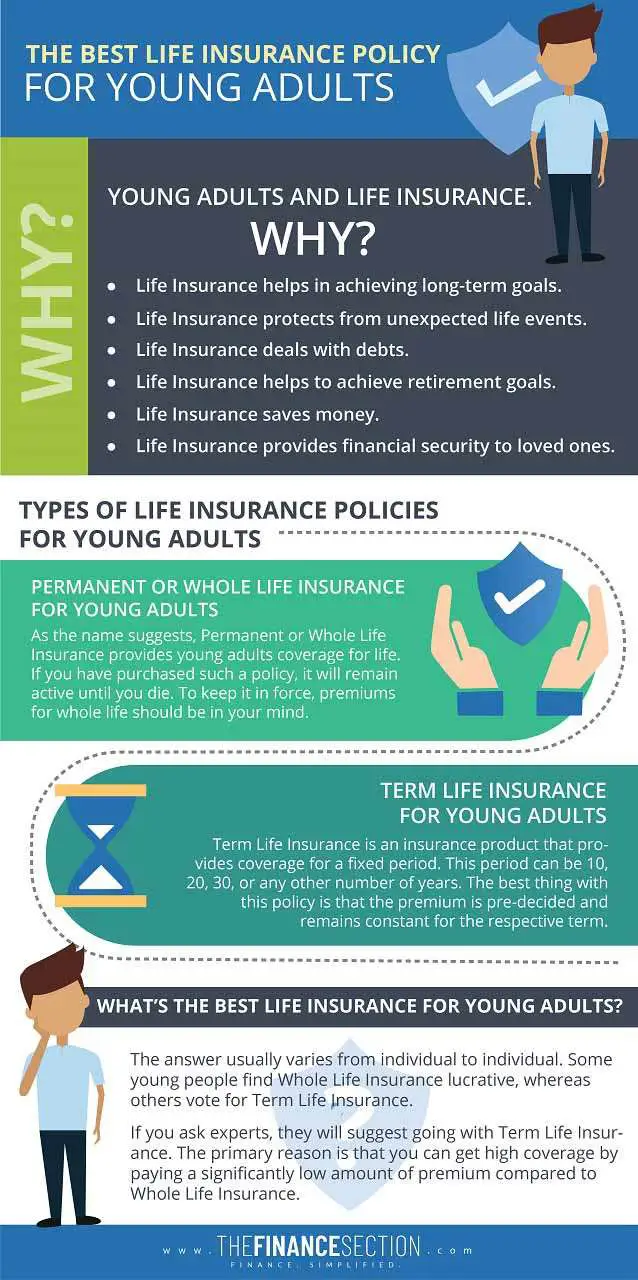

While it may seem unnecessary to think about life insurance at a young age, it is actually a wise financial decision. Life insurance provides a safety net for your loved ones in the event of your untimely demise. It can help cover funeral expenses, outstanding debts, and provide financial support to your family members or dependents.

Understanding Life Insurance for Young Adults

Life insurance is a contract between an individual and an insurance company. The policyholder pays regular premiums, and in return, the insurance company provides a lump sum payment, known as the death benefit, to the designated beneficiaries upon the policyholder's death. For young adults, life insurance offers financial protection during their early adult years when they may have financial obligations, such as student loans or starting a family.

The Benefits of Life Insurance for Young Adults

While it may be tempting to put off purchasing life insurance when you're young and healthy, there are several benefits to doing so. Firstly, obtaining life insurance at a young age typically means lower premiums. Insurance companies consider young adults to be lower risk, as they are generally healthier and less likely to have pre-existing medical conditions. Additionally, starting a life insurance policy early allows you to lock in lower rates for the duration of your coverage.

Another advantage of purchasing life insurance as a young adult is the peace of mind it provides. Knowing that your loved ones will be financially protected in the event of your passing can alleviate the stress and worry associated with unexpected circumstances. Life insurance can also serve as a financial tool, allowing you to leave a legacy or provide for charitable causes that are important to you.

Assessing Your Life Insurance Needs

Before diving into the various types of life insurance available, it's essential to assess your individual needs. Consider factors such as your current financial obligations, future goals, and the needs of your dependents. Start by calculating your debt, including student loans, credit card balances, and any other outstanding loans. You should also factor in your monthly living expenses, such as rent or mortgage payments, utilities, and groceries.

Next, think about your future goals. Do you plan on getting married, having children, or buying a home? These milestones often come with additional financial responsibilities, and life insurance can help provide for your loved ones in your absence. Finally, consider the needs of your dependents. If you have children, elderly parents, or other family members who rely on your income, life insurance can ensure they are financially supported if you were no longer there to provide for them.

Types of Life Insurance for Young Adults

When it comes to life insurance for young adults, there are several types of coverage to consider. Each type has its own features, benefits, and drawbacks. Understanding the differences between them will help you make an informed decision about which policy is right for you.

Term Life Insurance

Term life insurance provides coverage for a specific period, typically 10, 20, or 30 years. It is often the most affordable option for young adults. With term life insurance, you pay a fixed premium throughout the term, and if you pass away during that period, the death benefit is paid out to your beneficiaries. However, if you outlive the term, the coverage expires, and you will need to either renew the policy or seek alternative coverage.

Term life insurance is beneficial for young adults who have temporary financial obligations, such as a mortgage or student loans. It provides a safety net during the years when your loved ones may be most financially vulnerable. Additionally, term life insurance can be converted to permanent coverage in the future if your needs change or you want to continue having life insurance beyond the initial term.

Whole Life Insurance

Whole life insurance, also known as permanent life insurance, provides coverage for your entire lifetime, as long as premiums are paid. Unlike term life insurance, whole life insurance combines a death benefit with a cash value component. A portion of your premium goes towards building cash value, which grows over time on a tax-deferred basis.

One of the key benefits of whole life insurance is that it offers lifelong coverage, regardless of changes in your health or lifestyle. The cash value component also allows you to access funds through policy loans or withdrawals, providing a source of emergency funds or supplemental income in retirement. However, whole life insurance tends to have higher premiums than term life insurance, making it less affordable for some young adults.

Universal Life Insurance

Universal life insurance is another form of permanent coverage that provides a death benefit and a cash value component. It offers more flexibility than whole life insurance, allowing policyholders to adjust their premiums and death benefit amounts over time. Universal life insurance policies typically have a minimum premium requirement, and any excess premium payments go towards building cash value.

One of the advantages of universal life insurance is its flexibility. You can increase or decrease your death benefit or premium payments to adapt to changes in your financial situation or life circumstances. Universal life insurance also offers the potential for higher cash value accumulation, as the policy's cash value is invested in a variety of investment options. However, with the potential for investment gains comes the risk of investment losses, making universal life insurance a more complex option that requires careful consideration.

Factors to Consider When Choosing a Life Insurance Policy

Choosing the right life insurance policy can be overwhelming, but considering several key factors can help you make an informed decision based on your individual needs and circumstances.

Amount of Coverage

One of the first factors to consider is the amount of coverage you need. This will depend on various factors, including your current debts, future financial goals, and the needs of your dependents. A common rule of thumb is to aim for coverage that is at least 10 times your annual income. However, it's important to assess your unique situation and ensure that the coverage amount adequately provides for your loved ones in the event of your passing.

Policy Duration

The duration of your life insurance policy is another crucial consideration. If you have temporary financial obligations, such as a mortgage or student loans, a term life insurance policy that aligns with the duration of those obligations may be the most suitable option. On the other hand, if you want lifelong coverage and the ability to accumulate cash value, a permanent life insurance policy, such as whole life or universal life insurance, may be more appropriate.

Premium Affordability

When choosing a life insurance policy, it's essential to consider your budget and ensure that the premiums are affordable for the long term. While term life insurance generally has lower premiums, whole life and universal life insurance come with higher premium costs due to the lifelong coverage and cash value component. Carefully assess your financial situation and determine what premium amount you can comfortably afford without straining your budget.

Additional Policy Features

Life insurance policies can come with additional features and riders that provide added benefits and customization options. For example, some policies offer accelerated death benefit riders, which allow you to access a portion of the death benefit if you are diagnosed with a terminal illness. Other riders, such as disability income riders, provide supplemental income if you become disabled and unable to work. Consider these additional features and assess whether they align with your specific needs and priorities.

The Application Process for Life Insurance

Applying for life insurance involves several steps, and understanding the process can help make it smoother and more efficient.

Gather Relevant Documents

Before applying for life insurance, gather the necessary documents, such as proof of identity (e.g., driver's license or passport) and proof of income (e.g., pay stubs or tax returns). You may also need to provide information about your medical history, lifestyle habits, and any existing life insurance policies you have.

Understand Medical Examinations

Many life insurance policies require a medical examination to assess your health and determine your insurability. The examination typically includes a physical examination, blood tests, and sometimes a urine sample. It's important to be honest and thorough during the examination to ensure accurate underwriting and avoid potential issues with your coverage.

Complete the Application Form

Once you have gathered the necessary documents and completed the medical examination, it's time to fill out the application form. The application will ask for personal information, such as your name, address, and contact details. It will also require detailed information about your medical history, lifestyle habits, and any pre-existing conditions you may have.

Review and Sign the Policy

After completing the application, carefully review the policy documents provided by the insurance company. Ensure that all the information is accurate and matches what you discussed during the application process. If everything looks satisfactory, sign the policy documents, and submit them to the insurance company along with any required premium payments.

Tips for Finding Affordable Life Insurance Rates

Life insurance premiums can vary significantly depending on several factors, including your age,health, lifestyle, and the type of coverage you choose. Here are some tips to help you find affordable life insurance rates as a young adult:

Shop Around

Don't settle for the first life insurance policy you come across. Take the time to shop around and compare quotes from multiple insurance companies. Each company has its own underwriting guidelines and pricing strategies, so obtaining quotes from several providers will give you a better idea of the rates available to you.

Online comparison tools can be a valuable resource in your search for affordable life insurance. These tools allow you to enter your information once and receive quotes from multiple companies, making the comparison process more convenient and efficient.

Consider Term Life Insurance

Term life insurance is often the most affordable option for young adults. The premiums for term policies are generally lower than those for permanent policies because they provide coverage for a fixed period. If your primary concern is protecting your loved ones during your early adult years when financial obligations are high, term life insurance can offer the coverage you need at a more affordable price.

When considering term life insurance, be sure to choose a policy term that aligns with your specific needs. For example, if you have a 20-year mortgage, a 20-year term policy may provide the necessary coverage until your mortgage is fully paid off.

Maintain a Healthy Lifestyle

Your health plays a significant role in determining your life insurance premiums. Insurance companies assess your risk level based on factors such as your height and weight, medical history, and lifestyle habits. Adopting and maintaining a healthy lifestyle can help you secure lower rates.

Eat a balanced diet, exercise regularly, and avoid tobacco products. If you are a smoker, consider quitting as it can greatly impact your life insurance rates. Additionally, limit alcohol consumption and ensure you follow any prescribed medications or treatments for existing medical conditions.

Choose the Right Coverage Amount

The amount of coverage you choose directly affects your life insurance premiums. While it's important to have enough coverage to protect your loved ones, it's equally important not to overestimate your needs. Assess your financial obligations and the needs of your dependents to determine an appropriate coverage amount.

By accurately estimating your coverage needs, you can avoid paying for unnecessary coverage and potentially save on premiums. Remember, life insurance is designed to provide financial protection, not to serve as an investment vehicle, so be mindful of selecting a coverage amount that aligns with your specific requirements.

Consider Group Life Insurance

If you are employed, check if your employer offers group life insurance as part of your benefits package. Group life insurance policies often have lower premiums compared to individual policies because the risk is spread across a larger group of individuals.

While group life insurance can be a cost-effective option, it's important to note that the coverage amount may be limited and may not be portable if you leave your current job. Evaluate the terms and conditions of the group policy to ensure it meets your needs and consider supplementing it with an individual policy if necessary.

Review and Reassess Regularly

Life insurance is not a one-time decision. As your life circumstances change, it's important to review and reassess your coverage regularly. Life events such as marriage, the birth of a child, or purchasing a home can significantly impact your financial obligations and the coverage you require.

Take some time each year to evaluate your life insurance needs. Consider if your current policy is still sufficient or if adjustments need to be made. This proactive approach ensures that your coverage remains relevant and that you are not paying for unnecessary or inadequate protection.

Common Misconceptions about Life Insurance for Young Adults

There are several misconceptions surrounding life insurance for young adults. By debunking these myths, you can gain a better understanding of the importance and value of life insurance at a young age.

"I'm Young and Single, So I Don't Need Life Insurance"

While it's true that life insurance is often associated with individuals who have dependents, being young and single doesn't mean you should disregard life insurance. Even without dependents, you may still have financial obligations such as student loans, credit card debt, or funeral expenses that your loved ones would be responsible for if you were to pass away.

Moreover, purchasing life insurance at a young age can be a smart financial move. Premiums are generally lower when you are young and healthy, and by starting a policy early, you can lock in those lower rates for the duration of your coverage. This can save you money in the long run, especially if you plan to have dependents or anticipate financial responsibilities in the future.

"Life Insurance is Too Expensive for Young Adults"

Contrary to popular belief, life insurance can be affordable for young adults. The cost of life insurance is determined by various factors, including your age, health, lifestyle, and the type and amount of coverage you choose. As a young adult, you are likely to be in good health and have fewer pre-existing medical conditions, which can result in lower premiums.

By shopping around and comparing quotes from different insurance providers, you can find a policy that fits your budget. Additionally, opting for term life insurance can be a cost-effective choice, as it offers coverage for a specific period and generally has lower premiums than permanent policies.

"I Have Life Insurance through My Employer, so I'm Covered"

While employer-provided life insurance can be a valuable benefit, it's essential to understand the limitations and consider whether it provides sufficient coverage for your needs. Group life insurance policies offered by employers often have coverage amounts that are a multiple of your salary, which may not be enough to fully protect your loved ones in the event of your passing.

Furthermore, group life insurance typically ends when you leave your job, meaning you could lose coverage if you change employers or become self-employed. Having an individual life insurance policy ensures continuous coverage regardless of your employment status and allows you to customize the coverage to meet your specific needs.

Life Insurance Riders and Additional Coverage Options

In addition to the basic coverage provided by a life insurance policy, there are various riders and additional coverage options that you can consider to enhance your policy.

Accelerated Death Benefit Riders

An accelerated death benefit rider allows you to access a portion of the death benefit if you are diagnosed with a terminal illness. This rider can provide financial assistance to cover medical expenses or fulfill any final wishes you may have. It offers peace of mind, knowing that you can access the death benefit during your lifetime if needed.

Disability Income Riders

A disability income rider provides supplemental income if you become disabled and are unable to work. This rider can help maintain your financial stability by providing a regular income stream to cover living expenses and other financial obligations. It offers a layer of protection in the event that a disability prevents you from earning an income.

Waiver of Premium Riders

A waiver of premium rider waives future premium payments if you become disabled and are unable to work. This rider ensures that your life insurance coverage remains in force even if you are unable to afford the premiums due to a disability. It provides valuable protection and peace of mind during challenging times.

Child or Spousal Riders

Some life insurance policies offer the option to add child or spousal riders. These riders provide coverage for your children or spouse, typically at a lower cost than purchasing separate policies for each individual. Adding these riders can help ensure that your entire family is protected under a single policy.

Additional Coverage Options

In addition to riders, many insurance companies offer additional coverage options that can be tailored to your specific needs. These options may include coverage for critical illness, accidental death, or long-term care. Assess your individual circumstances and consider if any of these additional coverage options would provide valuable protection for you and your loved ones.

The Importance of Regularly Reviewing and Updating Your Policy

Life circumstances and financial needs can change over time, and it's important to regularly review and update your life insurance policy to ensure it continues to meet your evolving needs.

Life Events

Life events such as marriage, the birth of a child, or buying a home can significantly impact your financial obligations and the coverage you require. It's important to review your life insurance policy when these events occur to ensure that your coverage amount is sufficient to protect your loved ones.

Policy Renewal and Conversion

If you have a term life insurance policy, it's essential to be aware of the renewal process and conversion options. As your policy nears its expiration date, you may have the option to renew the coverage for an additional term or convert it into a permanent policy. Evaluate your current needs and circumstances to determine the best course of action.

Beneficiary Designations

Regularly review your beneficiary designations to ensure they reflect your current wishes. Life changes such as marriage, divorce, or the birth of a child may prompt you to update your beneficiaries. Keeping your beneficiary designations up to date ensures that the death benefit will be distributed according to your wishes.

Changes in Financial Situation

If your financial situation changes significantly, it's important to reassess your life insurance coverage. Consider factors such as changes in income, debts, orfinancial goals. If you experience a significant increase in income or accumulate more debt, you may need to adjust your coverage amount to adequately protect your loved ones. Similarly, if you pay off significant debts or experience a decrease in financial obligations, you may be able to reduce your coverage and potentially lower your premiums.

Consult with a Financial Advisor

If you're unsure about whether your current life insurance policy meets your needs or if you need assistance in reviewing and updating your coverage, consider consulting with a financial advisor. A financial advisor can provide valuable insights and guidance based on your specific situation and help you make informed decisions regarding your life insurance policy.

FAQs about Life Insurance for Young Adults

Here are answers to some frequently asked questions about life insurance for young adults:

Can I get life insurance if I have pre-existing health conditions?

Yes, you can still get life insurance if you have pre-existing health conditions. However, the premiums you pay may be higher, and the coverage options available to you may be limited. It's important to disclose any pre-existing conditions during the application process to ensure accurate underwriting and avoid potential issues with your coverage.

What happens if I miss a premium payment?

If you miss a premium payment, your policy may enter a grace period during which you can make the payment without any penalties or lapses in coverage. The length of the grace period varies depending on the insurance company and policy terms. If you fail to make the payment within the grace period, your policy may lapse, and you will no longer have coverage. It's important to pay your premiums on time to maintain continuous coverage.

Can I have multiple life insurance policies?

Yes, it is possible to have multiple life insurance policies. Having multiple policies can provide added flexibility and coverage options. For example, you may have a term life insurance policy to cover specific financial obligations and a permanent life insurance policy to provide lifelong coverage and accumulate cash value. However, it's important to assess your coverage needs and ensure that the total coverage amount is appropriate for your financial situation.

Can I change my life insurance policy in the future?

Yes, you can make changes to your life insurance policy in the future. Depending on the type of policy you have, you may have options such as converting a term policy into a permanent policy or adjusting the coverage amount. Keep in mind that any changes to your policy may be subject to underwriting and may result in changes to your premiums.

Is life insurance taxable?

In most cases, the death benefit received from a life insurance policy is not taxable. It is generally considered tax-free income for the beneficiaries. However, if the policyholder has a large estate, the death benefit may be subject to estate taxes. It's advisable to consult with a tax professional or financial advisor to understand the specific tax implications based on your individual circumstances.

Finding the Right Life Insurance Provider

Choosing the right life insurance provider is essential to ensure reliable coverage and excellent customer service. Here are some factors to consider when selecting an insurance company:

Financial Stability

Research the financial stability of the insurance company. Look for providers with strong financial ratings from reputable rating agencies. A financially stable company is more likely to fulfill its obligations and pay out claims when needed.

Customer Reviews and Reputation

Read customer reviews and testimonials to gauge the reputation of the insurance company. Look for feedback regarding customer service, claims processing, and overall satisfaction. A company with positive reviews and a good reputation is more likely to provide a positive experience.

Product Offerings and Customization Options

Consider the range of products and customization options offered by the insurance company. Look for providers that offer a variety of policy types and additional coverage options. This ensures that you can find a policy that aligns with your specific needs and goals.

Claims Process and Support

Research the claims process of the insurance company. Look for providers with a streamlined and efficient claims process. Additionally, consider the level of customer support provided. A company that offers excellent customer support can make the claims process smoother and less stressful.

Price and Affordability

Compare the prices and premiums offered by different insurance companies. While price should not be the sole determining factor, it is an important consideration. Evaluate the value offered for the price and ensure that the premiums are affordable for the coverage provided.

By considering these factors and conducting thorough research, you can find a life insurance provider that meets your needs and provides reliable coverage and excellent customer service.

In conclusion, life insurance is not just for older individuals; it is also essential for young adults. By understanding the basics, exploring the available options, and taking the necessary steps to secure a suitable policy, young adults can protect their loved ones and secure their financial future. Don't wait until it's too late – start exploring life insurance options today.

Post a Comment for "Life Insurance for Young Adults: A Comprehensive Guide"