Earthquake Insurance in High-Risk Regions: A Comprehensive Guide

Living in high-risk earthquake regions requires careful consideration and preparation. Earthquakes have the potential to cause significant damage to properties, leaving homeowners and businesses vulnerable to financial distress. In order to mitigate these risks, earthquake insurance is a crucial investment. This comprehensive guide aims to provide readers with a detailed understanding of earthquake insurance in high-risk regions, covering the importance of coverage, the types of policies available, and the factors to consider when purchasing a policy.

Earthquakes are unpredictable natural disasters that can strike at any time, making it essential for residents in high-risk regions to be adequately prepared. This blog article will serve as an informative resource, empowering readers to make informed decisions about earthquake insurance. By understanding the various aspects of earthquake insurance, individuals can protect their assets and financial well-being in the face of seismic events.

Understanding Earthquake Insurance: What It Covers and Why You Need It

In this section, we will delve into the fundamentals of earthquake insurance, providing readers with a comprehensive understanding of its coverage and the reasons why it is an essential investment for individuals residing in high-risk regions. Earthquakes can cause extensive damage to buildings, infrastructure, and personal belongings. This insurance coverage is specifically designed to protect against these risks, providing financial support to policyholders in the aftermath of an earthquake.

Comprehensive Coverage for Property and Belongings

Earthquake insurance typically covers a wide range of losses resulting from seismic events. This includes structural damage to buildings, such as foundations, walls, and roofs. It also extends coverage to personal belongings within the insured property, including furniture, appliances, and electronics. By having earthquake insurance, individuals can ensure that the cost of repairing or replacing these assets is covered, alleviating the financial burden that may arise from earthquake-related damage.

Additional Living Expenses

In the event that an earthquake renders a home uninhabitable, earthquake insurance often provides coverage for additional living expenses. This means policyholders can receive compensation for temporary accommodation, meals, and other necessary expenses while their home undergoes repairs. This coverage is crucial in enabling individuals to maintain their quality of life during the post-earthquake recovery period.

Protection Against Liability

Earthquakes can cause damage not only to a policyholder's property but also to neighboring properties. In these cases, earthquake insurance can provide liability coverage, protecting the policyholder from potential legal claims and associated costs. This coverage is particularly valuable in high-density areas where damage to multiple properties may occur due to seismic events.

Earthquake insurance is a necessity in high-risk regions due to the substantial financial implications of earthquake damage. Without proper coverage, individuals may face significant out-of-pocket expenses, which can lead to financial hardship and even bankruptcy. By investing in earthquake insurance, individuals can safeguard their assets and financial well-being, ensuring they have the necessary resources to recover from the aftermath of an earthquake.

Assessing Your Risk: Determining the Probability of Earthquakes in Your Area

Before purchasing earthquake insurance, it is essential to evaluate the level of risk in your specific region. Understanding the probability of earthquakes in your area allows you to assess the necessity and adequacy of earthquake insurance coverage. This section will provide readers with the necessary tools and resources to evaluate earthquake risk, enabling them to make informed decisions regarding insurance coverage.

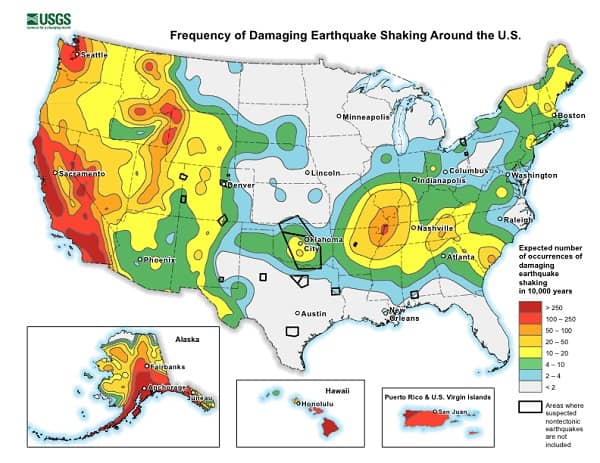

Seismic Hazard Maps

One of the key resources for assessing earthquake risk is seismic hazard maps. These maps provide valuable information about the likelihood of earthquakes occurring in specific regions. They take into account factors such as historical seismic activity, fault lines, and geological characteristics. By referring to these maps, individuals can gain a better understanding of the level of risk they face in their area.

Local Geological Surveys

Local geological surveys and organizations dedicated to studying seismic activity are another valuable resource for assessing earthquake risk. These entities conduct extensive research and analysis to determine the probability of earthquakes in specific regions. By accessing their findings and reports, individuals can gain insights into the seismic history and potential risks in their area.

Consulting with Experts

For a more comprehensive evaluation of earthquake risk, it may be beneficial to consult with experts in the field. Seismologists, geologists, and structural engineers can provide valuable insights and assessments based on their expertise and knowledge. These professionals can analyze factors such as soil composition, building codes, and vulnerability of existing structures, helping individuals make informed decisions about earthquake insurance coverage.

Understanding Regional Variations

It is important to note that earthquake risk can vary significantly within a region. Factors such as proximity to fault lines, soil conditions, and building standards can impact the likelihood and intensity of earthquakes. Therefore, it is crucial to consider localized risks when assessing earthquake insurance needs. Consulting with local authorities and experts familiar with regional variations can provide valuable insights into these localized risks.

By utilizing seismic hazard maps, consulting with experts, and understanding regional variations, individuals can gain a comprehensive understanding of the earthquake risk in their area. This knowledge serves as a foundation for making informed decisions about earthquake insurance coverage, ensuring that individuals are adequately protected against potential seismic events.

Types of Earthquake Insurance Policies: Understanding the Options Available

Earthquake insurance policies can vary in terms of coverage, cost, and the way they are structured. Understanding the different types of policies available is essential for selecting the coverage that best suits individual needs and preferences. This section will delve into the various options for earthquake insurance, providing readers with a comprehensive comparison to aid in their decision-making process.

Standalone Earthquake Insurance Policies

A standalone earthquake insurance policy is a dedicated policy that specifically covers earthquake-related damage. This type of policy is separate from a standard homeowner's insurance policy and provides comprehensive coverage for structural damage, personal belongings, and additional living expenses resulting from earthquakes. Standalone policies offer a higher degree of coverage and flexibility compared to endorsements or riders added to existing policies.

Endorsements or Riders

Some insurance providers offer endorsements or riders that can be added to existing homeowner's insurance policies to provide earthquake coverage. These endorsements enhance the existing policy by extending coverage to earthquake-related damage. While this option may be more convenient for individuals who already have a homeowner's insurance policy, it is important to carefully review the terms and limitations of the endorsement to ensure adequate coverage.

Government-Backed Earthquake Insurance Programs

In certain regions, government-backed earthquake insurance programs may be available. These programs are typically designed to provide affordable earthquake insurance coverage to residents in high-risk areas. Government-backed programs often offer competitive rates and comprehensive coverage, making them a viable option for individuals seeking earthquake insurance. It is important to research and understand the specific terms and eligibility criteria of these programs to determine if they are suitable.

Policy Limitations and Deductibles

When considering earthquake insurance options, it is crucial to carefully review the policy limitations and deductibles. Policy limitations outline what is covered and any exclusions or restrictions that may apply. Deductibles, on the other hand, determine the amount that the policyholder must pay out of pocket before the insurance coverage comes into effect. Understanding these aspects is essential for selecting a policy that aligns with individual needs and budget.

Comparing Coverage and Costs

Comparing the coverage and costs of different earthquake insurance policies is essential for making an informed decision. It is important to evaluate the extent of coverage provided, including structural damage, personal belongings, and additional living expenses. Additionally, comparing the costs of premiums and deductibles is crucial to ensure affordability. Obtaining quotes from multiple insurance providers and carefully reviewing the terms and conditions of each policy will help individuals make a well-informed choice.

By understanding the different types of earthquake insurance policies available, individuals can select coverage that is tailored to their specific needs. Whether opting for standalone policies, endorsements, or government-backed programs, it is important to carefully review policy details, limitations, and costs to ensure comprehensive coverage and financial protection.

Determining Coverage Limits: Calculating the Adequate Amount of Insurance

Choosing the right coverage limit is crucial to ensure adequate protection against earthquake damage. Underinsuring can leave individuals financially vulnerable, while overinsuring can lead to unnecessary expenses. This section will guide readers through the process of calculating the appropriate coverage limit based on factors such as property value, construction type, and personal belongings. It will also address common misconceptions about coverage limits and provide strategies for determining the most suitable coverage amount.

Property Value Assessment

Assessing the value of the property is an essential step in determining the appropriate coverage limit. This involves considering factors such as the current market value, replacement cost, and any unique features or upgrades that may affect the value. Consulting with real estate professionals or appraisers can provide valuable insights into accurately determining the property value.

Construction Type and Materials

The construction type and materials used in a property can significantly impact its vulnerability to earthquake damage. Certain construction methods and materials may be more resistant to seismic activity, reducing the potential for damage. Evaluating the construction type and materials, such as wood frame, reinforced concrete, or masonry, can help determine the appropriate coverage limit based on the property's susceptibility to earthquake damage.

Personal Belongings Inventory

Creating an inventory of personal belongings is crucial for accurately estimating the coverage needed for personal property. This involves

documenting all valuable items, including furniture, appliances, electronics, and other possessions. It is beneficial to include photographs, receipts, or appraisals to establish the value of these items. This inventory will serve as a reference point when determining the appropriate coverage limit for personal belongings.Consideration of Additional Structures

In addition to the main dwelling, it is important to consider any additional structures on the property, such as garages, sheds, or guest houses. These structures should be included in the overall coverage calculation to ensure that all assets are adequately protected in the event of an earthquake.

Understanding Coverage Percentage

Earthquake insurance policies often have coverage limits based on a percentage of the insured property's value. For example, a policy may offer coverage up to 80% of the property's value. It is crucial to understand and assess the coverage percentage offered by the policy to ensure that it aligns with the estimated replacement cost of the property.

Applying Deductibles

Deductibles play a significant role in earthquake insurance policies, as they determine the amount the policyholder must pay out of pocket before the insurance coverage kicks in. It is important to carefully consider the deductible amount and its impact on the overall coverage limit. Higher deductibles can result in lower premiums but may also increase the financial burden in the event of a claim.

Consulting with Insurance Professionals

Insurance professionals, such as agents or brokers, can provide valuable guidance in determining the appropriate coverage limit. They have experience in assessing risks and can help individuals navigate the complexities of coverage calculations. Consulting with these professionals can ensure that individuals select an appropriate coverage limit that aligns with their specific needs and budget.

By considering factors such as property value, construction type, personal belongings, and additional structures, individuals can accurately calculate the coverage limit needed for their earthquake insurance policy. It is important to review and update this coverage regularly to account for any changes in property value or possessions. By ensuring the coverage limit is adequate, individuals can have peace of mind knowing that their assets are protected in the event of an earthquake.

Exclusions and Limitations: Understanding What Is Not Covered

While earthquake insurance provides essential coverage, it is important to be aware of the exclusions and limitations of the policy. Understanding what is not covered can help individuals make informed decisions and take necessary precautions to protect their assets. This section will outline common exclusions, such as landslides and tsunamis, and explain coverage limitations for specific items or structures.

Exclusions: Landslides and Tsunamis

Many earthquake insurance policies do not cover damage resulting from landslides or tsunamis. These events, although often associated with earthquakes, are typically considered separate perils. It is important to understand the specific terms of the earthquake insurance policy to determine if coverage for these events is included or if separate insurance is necessary.

Structural and Material Limitations

Earthquake insurance policies may have limitations on coverage for certain types of structures or materials. For example, policies may exclude coverage for detached structures, such as fences or swimming pools, or may have lower coverage limits for masonry or unreinforced buildings. It is crucial to carefully review the policy terms to understand these limitations and consider any additional coverage that may be necessary.

Personal Property Sub-Limits

While earthquake insurance policies generally cover personal property, there may be sub-limits or coverage caps for specific categories of items. For example, policies may limit coverage for jewelry, artwork, or collectibles. It is important to review these sub-limits and consider additional endorsements or separate policies to adequately protect valuable or high-value items.

Waiting Periods

Some earthquake insurance policies have waiting periods, which means that coverage does not take effect immediately after purchasing the policy. Waiting periods can range from a few days to several weeks or months. It is crucial to be aware of any waiting periods in the policy and plan accordingly to ensure coverage when it is needed.

Secondary Damage Exclusions

Earthquakes can cause secondary damage, such as fires or water damage from burst pipes. Some earthquake insurance policies may not cover these secondary damages directly but may provide coverage for the resulting damage if it is a named peril in the policy. It is important to understand the relationship between earthquake coverage and coverage for secondary perils to ensure comprehensive protection.

Reviewing Policy Endorsements or Riders

Endorsements or riders added to earthquake insurance policies can modify the coverage and introduce additional exclusions or limitations. It is crucial to carefully review the terms and conditions of any endorsements or riders attached to the policy to understand their impact on coverage. Consulting with insurance professionals can provide clarity and help individuals make informed decisions.

By understanding the exclusions and limitations of earthquake insurance policies, individuals can take necessary precautions and consider additional coverage options to protect their assets fully. It is important to review policy terms and conditions carefully and seek clarification from insurance professionals when needed.

Deductibles: How Much You Will Pay Out of Pocket

Deductibles play a crucial role in earthquake insurance policies, as they determine the amount that the policyholder must pay out of pocket before the insurance coverage comes into effect. It is essential to understand the different types of deductibles and carefully consider the deductible amount when purchasing earthquake insurance. This section will explain the different types of deductibles, such as percentage deductibles and fixed deductibles, and provide guidance on choosing the deductible amount that aligns with individual financial capabilities.

Percentage Deductibles

Percentage deductibles are calculated based on a percentage of the insured property's value. For example, if the insured property is valued at $500,000 and the policy has a 5% deductible, the policyholder would be responsible for paying the first $25,000 of any earthquake-related damage. Percentage deductibles are commonly used in earthquake insurance policies and can vary depending on the policy and the insurer.

Fixed Deductibles

Fixed deductibles, also known as flat deductibles, are a predetermined dollar amount that the policyholder must pay out of pocket before the insurance coverage applies. Unlike percentage deductibles, fixed deductibles do not fluctuate based on the property's value. Policyholders with fixed deductibles will be responsible for paying the full predetermined amount before receiving compensation for earthquake-related damage.

Choosing the Right Deductible Amount

When choosing a deductible amount, it is important to consider individual financial capabilities. While higher deductibles may lower the insurance premium, they also increase the out-of-pocket expenses in the event of a claim. It is essential to strike a balance between a deductible that is financially manageable and a premium that remains affordable.

Assessing Risk Tolerance

Individuals should assess their risk tolerance when determining the deductible amount. Consider factors such as the likelihood of earthquakes in the area, the potential severity of earthquake damage, and personal financial stability. Those with a higher risk tolerance may be comfortable with a higher deductible to reduce premium costs, while those with a lower risk tolerance may opt for a lower deductible to minimize out-of-pocket expenses.

Budgeting for Deductible Payments

It is crucial to budget and plan for the potential payment of deductibles. Earthquake-related damage can be costly, and individuals should ensure that they have the financial means to cover their deductible amount in the event of a claim. Setting aside funds specifically for deductible payments can provide peace of mind and ensure preparedness.

Reevaluating Deductible Amounts

Individuals should periodically reevaluate their deductible amounts as their financial situation changes. Adjustments may be necessary if there are significant changes in income, savings, or other financial circumstances. It is also important to review and understand any changes in deductible amounts when renewing an earthquake insurance policy.

By understanding the different types of deductibles and considering individual financial capabilities and risk tolerance, individuals can select the deductible amount that aligns with their needs. Careful consideration of deductibles ensures that individuals are prepared for potential out-of-pocket expenses while maintaining affordable earthquake insurance coverage.

Comparing Insurance Providers: Choosing the Right Company

With numerous insurance providers offering earthquake insurance, selecting the right company can be overwhelming. The choice of insurance provider is crucial, as it determines the reliability and quality of the coverage. This section will provide readers with guidance on evaluating insurance providers, considering factors such as financial stability, customer service, claims handling, and reputation. By making an informed decision when selecting their insurance provider, individuals can have confidence in their earthquake insurance coverage.

Evaluating Financial Stability

Financial stability is a key factor to consider when evaluating insurance providers. An insurance company's financial strength indicates its ability to fulfill its obligations in the event of a large-scale earthquake and subsequent claims. Evaluating an insurer's financial ratings, such as those provided by rating agencies like A.M. Best or Standard & Poor's, can provide insights into their stability and financial standing.

Assessing Claims Handling Process

The claims handling process is a critical aspect of an insurance provider's service. When filing a claim, individuals want reassurance that their insurer will handle it efficiently and fairly. Researching and reviewing an insurance provider's claims handling process, including customer reviews and testimonials, can provide valuable insights into their responsiveness andefficiency in handling earthquake-related claims. It is important to consider factors such as the ease of filing claims, the speed of claims processing, and the overall customer satisfaction with the claims experience.

Customer Service and Support

Good customer service is essential when dealing with insurance providers. Assessing the level of customer service and support offered by insurance companies is crucial for a smooth and satisfactory experience. This includes factors such as accessibility of customer support channels, responsiveness to inquiries, and the willingness to provide guidance and assistance throughout the insurance process.

Reputation and Reviews

Considering an insurance provider's reputation and reviews can provide valuable insights into their overall performance and customer satisfaction. Researching online reviews, seeking recommendations from trusted sources, and checking consumer advocacy websites can help individuals gauge the reputation of insurance providers. It is important to consider both positive and negative reviews to get a balanced perspective.

Policy Options and Flexibility

Insurance providers that offer a range of policy options and flexibility can cater to individual needs and preferences. Assessing the variety of coverage options, limits, deductibles, and additional endorsements provided by insurance companies is important for finding a policy that meets specific requirements. Flexibility in adjusting coverage as needs change is also a desirable feature to consider.

Availability of Discounts and Bundling Options

Some insurance providers offer discounts or bundling options that can help reduce premiums or provide added value. It is worth exploring if an insurance company offers discounts for bundling earthquake insurance with other policies, such as homeowner's insurance. Additionally, discounts based on factors like home security systems or retrofitted buildings can also contribute to cost savings.

Seeking Recommendations and Expert Advice

Seeking recommendations from friends, family, or trusted professionals in the insurance industry can provide valuable insights and guidance when choosing an insurance provider. Experts, such as insurance brokers or agents, can also provide personalized advice based on individual needs and preferences. Consulting with these experts can help individuals make an informed decision based on their unique circumstances.

By carefully evaluating insurance providers based on their financial stability, claims handling process, customer service, reputation, policy options, and available discounts, individuals can make an informed decision when selecting their earthquake insurance provider. It is important to conduct thorough research and consider multiple factors to ensure that the chosen insurance company is reliable and capable of providing the necessary coverage and support in the event of an earthquake.

Premiums and Affordability: Balancing Coverage and Cost

While earthquake insurance is vital for protecting against seismic events, it is essential to strike a balance between comprehensive coverage and affordability. Premiums play a significant role in earthquake insurance, as they determine the cost of coverage. This section will explore the factors that influence earthquake insurance premiums, such as location, construction type, coverage limits, and deductibles. By understanding these factors, individuals can manage costs while maintaining adequate coverage.

Location and Seismic Risk

The location of a property in relation to seismic activity is a primary factor in determining earthquake insurance premiums. High-risk regions with a history of earthquakes or proximity to fault lines generally have higher premiums due to the increased likelihood of earthquake-related damage. Individuals should be prepared for potentially higher premiums if they reside in these areas.

Construction Type and Building Materials

The type of construction and building materials used in a property can influence earthquake insurance premiums. Buildings with reinforced structures or materials that are more resistant to seismic activity may have lower premiums due to their reduced vulnerability. On the other hand, buildings with outdated or less resilient construction may result in higher premiums.

Coverage Limits and Deductibles

The coverage limits and deductibles selected for an earthquake insurance policy can have an impact on premiums. Higher coverage limits and lower deductibles generally result in higher premiums, as they provide more comprehensive protection and reduce out-of-pocket expenses for the policyholder. Individuals should consider their risk tolerance and financial capabilities when selecting coverage limits and deductibles.

Loss History and Insurance Claims

Insurance companies take into account the loss history and insurance claims of a region when determining premiums. Areas with a higher frequency or severity of earthquake damage may experience higher premiums. It is essential to be aware of the historical earthquake activity in the region and understand how it may impact insurance premiums.

Discounts and Risk Mitigation Measures

Some insurance companies offer discounts or incentives for risk mitigation measures that reduce the potential for earthquake damage. This can include retrofitting the property, installing seismic safety measures, or implementing other protective measures. Individuals should inquire about potential discounts or incentives that may help reduce premiums while improving the property's resilience to earthquakes.

Comparing Quotes and Policy Options

Obtaining quotes from multiple insurance providers and comparing policy options is crucial for managing costs. This allows individuals to evaluate the premiums, deductibles, coverage limits, and additional features offered by different insurers. It is important to consider the overall value and coverage provided, rather than solely focusing on the premium amount.

By understanding the factors that influence earthquake insurance premiums and taking proactive measures to mitigate risk, individuals can strike a balance between comprehensive coverage and affordability. It is essential to consider multiple factors and obtain quotes from various insurance providers to ensure that the selected policy offers adequate protection at a reasonable cost.

Additional Mitigation Measures: Supplementing Insurance with Protective Actions

While earthquake insurance provides essential financial protection, it is crucial to supplement it with additional mitigation measures. Proactive actions can reduce the potential impact of earthquakes and enhance overall preparedness. This section will highlight various mitigation measures that individuals can take to complement their insurance coverage, such as retrofitting homes, securing furniture, and creating emergency plans.

Retrofitting Homes

Retrofitting homes involves reinforcing the structure to make it more resistant to seismic activity. This can include adding bracing to walls, strengthening foundations, or securing chimneys. Retrofitting measures can significantly reduce the risk of structural damage during an earthquake and minimize potential repair costs. Hiring a professional structural engineer can provide guidance on the most effective retrofitting measures for individual properties.

Securing Furniture and Belongings

During an earthquake, unsecured furniture and belongings can become hazards, causing injuries or damage. Securing heavy furniture, appliances, and valuable items can minimize the risk of them toppling over or falling during seismic events. Simple measures such as installing brackets, straps, or latches can help secure these items and provide added protection.

Creating Emergency Plans

Having a well-prepared emergency plan is essential for ensuring the safety of individuals and their households during an earthquake. This plan should include procedures for evacuation, a designated meeting point, and communication strategies. It is important to regularly review and practice the emergency plan with all household members to ensure everyone is familiar with the necessary steps to take in the event of an earthquake.

Stocking Emergency Supplies

Preparing an emergency supply kit with essential items is crucial for surviving the aftermath of an earthquake. This kit should include items such as non-perishable food, water, first aid supplies, flashlights, batteries, and a portable radio. It is important to periodically check and replenish the supplies to ensure they are up to date and readily available in case of an emergency.

Participating in Community Preparedness Programs

Communities often have preparedness programs and resources aimed at educating residents about earthquake safety and mitigation measures. Participating in these programs can provide valuable information, training, and resources to enhance individual and community preparedness. It is advisable to connect with local authorities or organizations to learn about available programs and initiatives.

Regular Property Maintenance

Regular property maintenance is crucial for identifying and addressing potential vulnerabilities that could exacerbate earthquake damage. Conducting routine inspections, repairing structural issues, and addressing any signs of deterioration can help minimize the impact of earthquakes. It is important to prioritize maintenance efforts to ensure the property remains resilient and less susceptible to damage.

By supplementing earthquake insurance with these additional mitigation measures, individuals can enhance their overall preparedness and reduce the potential impact of earthquakes. Taking proactive actions to secure the property, create emergency plans, and participate in community preparedness programs contributes to a safer environment and better protection against seismic events.

Frequently Asked Questions: Addressing Common Queries and Concerns

Addressing common questions and concerns about earthquake insurance is essential for providing readers with a comprehensive understanding of the topic. This section will answer frequently asked queries, clarifying doubts and providing additional insights. By addressing these questions, individuals can gain a better understanding of earthquake insurance and make informed decisions regarding their coverage.

1. Is earthquake insurance mandatory in high-risk regions?

No, earthquake insurance is typically not mandatory. However, it is highly recommended for individuals residing in high-risk regions due to the potential financial implications of earthquake damage.

2. Will my homeowner's insurance policy cover earthquake damage?

Most standard homeowner's insurance policies do not cover earthquake damage. Separate earthquake insurance or endorsements are typically required to have coverage for seismic events.

3. Are all earthquake insurance policies the same?

No, earthquake insurance policies can vary in terms of coverage, deductibles, and limitations. It is important to review the policy details and compare options to select coverage that suits individual needs.

4. Can earthquake insurance cover all personal belongings?

Earthquake insurance policies generally provide coverage for personal belongings within the insured property. However, there may be sub-limits or exclusions for certain categories of items, such as jewelry, artwork, or collectibles. It is important to review the policy terms and consider additional coverage options if necessary to ensure adequate protection for valuable or high-value items.

5. Will earthquake insurance cover temporary accommodation expenses?

Yes, earthquake insurance often includes coverage for additional living expenses. This means that if your home becomes uninhabitable due to earthquake damage, the insurance policy can provide compensation for temporary accommodation, meals, and other necessary expenses until your home is repaired or rebuilt.

6. Can I purchase earthquake insurance if I rent a property?

Yes, earthquake insurance is available for renters as well. Renter's earthquake insurance can provide coverage for personal belongings and additional living expenses in the event of earthquake damage to the rented property.

7. What factors determine earthquake insurance premiums?

Earthquake insurance premiums are determined by various factors, including the location of the property, construction type, coverage limits, deductibles, and the insurer's underwriting criteria. High-risk regions, older buildings, higher coverage limits, and lower deductibles generally result in higher premiums.

8. Can I add earthquake coverage to my existing homeowner's insurance policy?

Yes, some insurance providers offer endorsements or riders that can be added to existing homeowner's insurance policies to provide earthquake coverage. It is important to review the terms and limitations of these endorsements and ensure they provide adequate coverage for your needs.

9. How soon after purchasing earthquake insurance does the coverage take effect?

Most earthquake insurance policies have a waiting period, which is the period of time that must pass before coverage takes effect. Waiting periods can vary, typically ranging from a few days to several weeks or months. It is important to be aware of the waiting period specified in your policy.

10. Can I cancel or change my earthquake insurance policy?

Yes, you can typically cancel or make changes to your earthquake insurance policy. However, it is important to review the terms and conditions of the policy and consult with your insurance provider to understand any potential penalties or restrictions associated with policy cancellation or modifications.

By addressing these frequently asked questions, individuals can gain a better understanding of earthquake insurance and make informed decisions regarding their coverage. It is important to review policy details, consult with insurance professionals, and seek clarification when needed to ensure comprehensive protection against earthquake-related risks.

In conclusion, earthquake insurance is a crucial component of financial preparedness for individuals residing in high-risk regions. By understanding the coverage provided, evaluating the level of seismic risk, comparing policy options, and considering personal needs and budget, individuals can make informed decisions to protect their assets and mitigate potential financial losses in the event of an earthquake. It is important to remember that earthquake insurance should be supplemented with proactive measures, such as retrofitting homes, securing belongings, creating emergency plans, and participating in community preparedness programs. By taking a comprehensive approach to earthquake preparedness, individuals can enhance their resilience and navigate the challenges posed by earthquakes with greater peace of mind.

Post a Comment for "Earthquake Insurance in High-Risk Regions: A Comprehensive Guide"